#Application Delivery Controller Market Analysis

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Forty percent of Tumblr users are between the ages of 18 to 25.

Text

Key Trends and Innovations Driving Application Delivery Controller Market

The global application delivery controller (ADC) market was valued at USD 4.35 billion in 2024 and is projected to experience a strong growth trajectory, expanding at a compound annual growth rate (CAGR) of 12.9% from 2025 to 2030. ADCs are integral components in modern IT infrastructures, used to manage and optimize the delivery of applications across complex and dynamic environments, ensuring they remain highly available, secure, and perform at their peak.

The increasing frequency and sophistication of cyber threats has made application security one of the foremost concerns for organizations across industries. Cyberattacks targeting web applications and networks can result in significant financial losses, data breaches, and reputational damage. As organizations face mounting pressure to protect their applications, ADCs with robust security features like DDoS protection, WAFs, and intrusion prevention systems (IPS) have become indispensable

The ongoing expansion of the Internet of Things (IoT) ecosystem is another critical factor driving the demand for ADCs. With billions of IoT devices being connected to networks globally, there is a massive increase in the amount of data generated, which needs to be managed efficiently. ADCs play a pivotal role in ensuring that this influx of data can be handled without compromising application performance. ADCs are essential for managing and optimizing traffic between IoT devices and centralized data processing systems, ensuring that applications run smoothly even as the volume and complexity of data grow.

Furthermore, edge computing—where data is processed closer to the source rather than in centralized data centers—is becoming increasingly important for IoT and other latency-sensitive applications. ADCs can support edge computing environments by efficiently managing traffic across distributed locations, ensuring low-latency access to applications and services for end-users. As more enterprises adopt edge computing, the demand for ADCs that can seamlessly handle traffic in such distributed environments will continue to rise.

Gather more insights about the market drivers, restrains and growth of the Application Delivery Controller Market

Regional Insights

North America: Leading the ADC Market

In 2024, North America held the largest share of the global Application Delivery Controller (ADC) market, accounting for over 34% of the total market revenue. This region is a key driver of market growth due to its advanced technological infrastructure, especially in the U.S. and Canada, where enterprises are at the forefront of cloud adoption and digital transformation. As businesses increasingly move towards hybrid and multi-cloud environments, the demand for ADCs has risen substantially.

In these cloud-based environments, ADCs are essential for optimizing application delivery. They help manage network traffic, ensuring scalability, high availability, and secure data flow across diverse infrastructures. ADCs are crucial for optimizing the performance of cloud applications, balancing traffic, and reducing latency, which is especially important as organizations depend more on cloud services to improve operational efficiency. This growing reliance on cloud technologies contributes to the increasing demand for ADC solutions that can integrate seamlessly across various platforms. As such, North America remains a key growth market for ADC providers, with companies seeking solutions that can handle dynamic workloads while maintaining high performance and security in their digital transformation initiatives.

U.S. Application Delivery Controller Market Trends

The U.S. ADC market maintained a dominant position in 2024 and is expected to continue to lead the market through the forecast period. The U.S. has seen substantial growth in sectors such as e-commerce and digital services, particularly within retail and financial services. As these online platforms face ever-increasing volumes of traffic, ensuring efficient application performance becomes crucial. ADCs play a vital role by optimizing application performance, minimizing latency, and providing scalability to manage traffic during peak demand periods. For instance, during events like sales promotions or market fluctuations, ADCs ensure reliable access and smooth user experiences. This growing reliance on digital platforms is further fueling the demand for ADC solutions, propelling market growth across the region.

Asia Pacific: Rapid Growth and Digital Transformation

The Asia Pacific (APAC) region is expected to witness significant growth in the ADC market, with a CAGR of 14.2% from 2025 to 2030. In this region, small and medium-sized enterprises (SMEs) are rapidly adopting digital technologies and cloud services to improve their operations. As these businesses expand their digital presence, they increasingly require scalable and cost-effective ADC solutions to maintain reliable performance and efficient traffic management, especially as their digital workloads grow. The adoption of virtual ADCs is a key factor in this shift, as they provide affordable and flexible solutions for SMEs seeking to stay competitive in the increasingly digital economy, all while ensuring high security and performance standards.

Japan

Additionally, Japan's application delivery controller market is expected to grow rapidly, driven by the country's focus on advanced technologies like AI and IoT. These technologies require the efficient management of complex application environments, and ADCs are essential to ensuring optimal performance, scalability, and seamless integration across various platforms and systems.

China

China's ADC market also held a substantial share in 2024, with growth driven by the country’s accelerated digital transformation across key sectors such as manufacturing, finance, and healthcare. As these sectors digitize their operations, they increasingly depend on ADCs to optimize application performance, streamline operations, and ensure reliable, seamless delivery of services in complex environments.

Europe: Rising Demand Amid Security Concerns

Europe

In Europe, the ADC market is growing steadily, fueled by increasing cybersecurity threats across the region. As organizations face rising risks from cyberattacks, they are increasingly investing in ADCs that offer advanced security features to safeguard sensitive data. ADCs integrate threat protection capabilities that help mitigate risks, ensuring secure application performance and compliance with regulatory standards in an increasingly complex digital landscape.

U.K.

The U.K. ADC market is set to see rapid growth due to the increasing adoption of cloud services across industries. As businesses deploy hybrid and multi-cloud environments, there is a rising need for ADCs to manage traffic efficiently and ensure optimal performance and reliability. ADCs also enable seamless integration and communication between applications, ensuring that cloud-based services remain highly available and secure across different platforms.

Germany

In Germany, the ADC market is also expected to hold a significant market share in the coming years. Germany's strong manufacturing and IT sectors are fueling demand for ADC solutions. These industries rely on ADCs to optimize application delivery and performance, enhance operational efficiency, and maintain seamless communication across complex IT environments. The demand for ADCs in sectors like automotive, chemicals, and pharmaceuticals will continue to drive the market as companies seek to improve their digital infrastructures.

Browse through Grand View Research's Network Security Industry Research Reports.

• The global IoT security market size was valued at USD 35.50 billion in 2024 and is projected to grow at a CAGR of 26.8% from 2025 to 2030.

• The global data center security market was valued at USD 18.42 billion in 2024 and is projected to grow at a CAGR of 16.8% from 2025 to 2030.

Key Insights on ADC Market Players

Some of the key players driving innovation and competition in the ADC market include F5 Networks, A10 Networks, Citrix Systems, and Barracuda Networks. These companies are adopting several strategic initiatives, such as mergers and acquisitions, partnerships, and expansion into new markets, to increase their customer base and enhance their market position.

F5 Networks is well-known for its advanced ADC solutions that optimize the performance, security, and scalability of applications across both multi-cloud and on-premises environments. F5’s ADCs help businesses ensure application availability, secure traffic management, and flexible load balancing. As cloud computing continues to grow, F5's innovations, particularly around integrating ADCs with security features like Web Application Firewalls (WAF), have positioned the company as a critical player in supporting businesses undergoing digital transformation.

Citrix Systems is another key player with its NetScaler ADC solutions, which are designed to optimize load balancing, application acceleration, and security. Citrix ADCs are widely used in cloud and on-premises environments and are popular among enterprises looking to improve their application delivery. These products are integral to helping businesses scale effectively while maintaining high levels of performance and security.

Key Application Delivery Controller Companies:

The following are the leading companies in the application delivery controller market. These companies collectively hold the largest market share and dictate industry trends.

• F5 Networks

• A10 Networks

• Citrix Systems

• Radware

• Array Networks

• Kemp Technologies

• Fortinet, Inc.

• Cisco Systems

• Barracuda Networks

• ZEVENET

Order a free sample PDF of the Application Delivery Controller Market Intelligence Study, published by Grand View Research.

#Application Delivery Controller Market#Application Delivery Controller Market Analysis#Application Delivery Controller Market Report#Application Delivery Controller Industry

0 notes

Text

Gemini Code Assist Enterprise: AI App Development Tool

Introducing Gemini Code Assist Enterprise’s AI-powered app development tool that allows for code customisation.

The modern economy is driven by software development. Unfortunately, due to a lack of skilled developers, a growing number of integrations, vendors, and abstraction levels, developing effective apps across the tech stack is difficult.

To expedite application delivery and stay competitive, IT leaders must provide their teams with AI-powered solutions that assist developers in navigating complexity.

Google Cloud thinks that offering an AI-powered application development solution that works across the tech stack, along with enterprise-grade security guarantees, better contextual suggestions, and cloud integrations that let developers work more quickly and versatile with a wider range of services, is the best way to address development challenges.

Google Cloud is presenting Gemini Code Assist Enterprise, the next generation of application development capabilities.

Beyond AI-powered coding aid in the IDE, Gemini Code Assist Enterprise goes. This is application development support at the corporate level. Gemini’s huge token context window supports deep local codebase awareness. You can use a wide context window to consider the details of your local codebase and ongoing development session, allowing you to generate or transform code that is better appropriate for your application.

With code customization, Code Assist Enterprise not only comprehends your local codebase but also provides code recommendations based on internal libraries and best practices within your company. As a result, Code Assist can produce personalized code recommendations that are more precise and pertinent to your company. In addition to finishing difficult activities like updating the Java version across a whole repository, developers can remain in the flow state for longer and provide more insights directly to their IDEs. Because of this, developers can concentrate on coming up with original solutions to problems, which increases job satisfaction and gives them a competitive advantage. You can also come to market more quickly.

GitLab.com and GitHub.com repos can be indexed by Gemini Code Assist Enterprise code customisation; support for self-hosted, on-premise repos and other source control systems will be added in early 2025.

Yet IDEs are not the only tool used to construct apps. It integrates coding support into all of Google Cloud’s services to help specialist coders become more adaptable builders. The time required to transition to new technologies is significantly decreased by a code assistant, which also integrates the subtleties of an organization’s coding standards into its recommendations. Therefore, the faster your builders can create and deliver applications, the more services it impacts. To meet developers where they are, Code Assist Enterprise provides coding assistance in Firebase, Databases, BigQuery, Colab Enterprise, Apigee, and Application Integration. Furthermore, each Gemini Code Assist Enterprise user can access these products’ features; they are not separate purchases.

Gemini Code Support BigQuery enterprise users can benefit from SQL and Python code support. With the creation of pre-validated, ready-to-run queries (data insights) and a natural language-based interface for data exploration, curation, wrangling, analysis, and visualization (data canvas), they can enhance their data journeys beyond editor-based code assistance and speed up their analytics workflows.

Furthermore, Code Assist Enterprise does not use the proprietary data from your firm to train the Gemini model, since security and privacy are of utmost importance to any business. Source code that is kept separate from each customer’s organization and kept for usage in code customization is kept in a Google Cloud-managed project. Clients are in complete control of which source repositories to utilize for customization, and they can delete all data at any moment.

Your company and data are safeguarded by Google Cloud’s dedication to enterprise preparedness, data governance, and security. This is demonstrated by projects like software supply chain security, Mandiant research, and purpose-built infrastructure, as well as by generative AI indemnification.

Google Cloud provides you with the greatest tools for AI coding support so that your engineers may work happily and effectively. The market is also paying attention. Because of its ability to execute and completeness of vision, Google Cloud has been ranked as a Leader in the Gartner Magic Quadrant for AI Code Assistants for 2024.

Gemini Code Assist Enterprise Costs

In general, Gemini Code Assist Enterprise costs $45 per month per user; however, a one-year membership that ends on March 31, 2025, will only cost $19 per month per user.

Read more on Govindhtech.com

#Gemini#GeminiCodeAssist#AIApp#AI#AICodeAssistants#CodeAssistEnterprise#BigQuery#Geminimodel#News#Technews#TechnologyNews#Technologytrends#Govindhtech#technology

3 notes

·

View notes

Text

Opioids Market Global Industry Analysis and Forecast (2023-2032)

Market Overview –

The opioids market is predicted to grow at a 5.4% CAGR between 2023 and 2032, reaching USD 6.93 billion.

The Opioids Market encompasses pharmaceutical drugs derived from opium or synthesized to mimic its effects, primarily used for pain management. Opioids are potent analgesics commonly prescribed for acute and chronic pain conditions, including postoperative pain, cancer-related pain, and severe injuries. However, the widespread use of opioids has led to concerns about addiction, overdose, and misuse.

The opioids market, while grappling with addiction concerns, sees a promising trend with the growing adoption of naltrexone. This medication offers a novel approach to managing opioid dependence by blocking opioid receptors, reducing cravings and withdrawal symptoms. As awareness rises, naltrexone's role in addiction treatment strengthens, contributing to a multifaceted approach to opioid management.

In recent years, the opioids market has witnessed significant growth globally due to several factors. Firstly, there has been increasing recognition of the need for effective pain management options, particularly in the context of aging populations and rising prevalence of chronic pain conditions. Key players in this market include pharmaceutical companies, healthcare providers, pain management clinics, and regulatory agencies, collaborating to develop and distribute opioids responsibly while mitigating risks of abuse and addiction.

Moreover, advancements in opioid formulations and delivery systems have led to the development of extended-release, abuse-deterrent, and non-opioid combination products. These innovations aim to improve pain control, reduce side effects, and minimize the potential for addiction and misuse.

Segment analysis

The segment study for the global opioids market is done by product, end-users, and applications. The product based segments of the opioids market are immediate-release/short-acting opioids and extended-release/long-acting opioids. The sub-segments of the extended-release opioid segment are morphine, oxycodone, oxymorphone, and hydromorphone among others. The extended-release opioid segment can value above USD 12,750.91 Mn by 2027. The sub-segments of the immediate-release opioid segment are hydrocodone, codeine, morphine, and fentanyl among others. The application-based segments of the opioids market are anesthesia, pain relief, diarrhoea suppression, cough suppression, and de-addiction. The end-user based segments of the global opioids market are pharmacies, academic research institutes, and hospitals & clinics. The end-user segments can largely benefit the opioids market.

Regional Analysis

The opioids market in Americas can secure the largest share of the worldwide global opioids market in the study period. The increase in the application of intravenous usage of opioids due to its fast action can promote the regional market rise in the near future. The growing awareness of IV application of opioids and its medical uses can drive the regional market in the near future. The market in Americas can accounted for the major share of the worldwide opioids market owing due rise in intravenous drug application. In Europe, the opioids market can thrive owing to the rise in demand for palliative care facilities. The introduction of reformed regulations for prescribing opioids can promote the market in the region. In Asia Pacific, the market is likely to be fast growing through the review period. Populace demographics and rise in availability of effective opioid medicines can favor the Asia Pacific opioids market in the analysis period. In South Korea, the market can secure about 6% of the APAC opioids market by 2027. In the Middle East and Africa region, a steady rise for the market is likely due to increase in count of opioid manufacturers in the region.

Key Players –

Opioids key players include Sanofi from France, Teva Pharmaceutical Industries from Israel, Bristol-Myers Squibb from the US, AbbVie Inc. from the US, Boehringer Ingelheim International GmbH from Germany, Purdue Pharma from the US, Astellas Pharma Inc. from Japan, Pfizer Inc. from the US, Biogen Idec from the US, Bayer from Germany, and GlaxoSmithKline from the UK.

Related Reports –

amniotic membrane market

asia pacific aesthetics market

diabetic nephropathy market

chronic kidney disease market

For more information visit at MarketResearchFuture

2 notes

·

View notes

Text

Data Science Unveiled: A Journey Across Industries

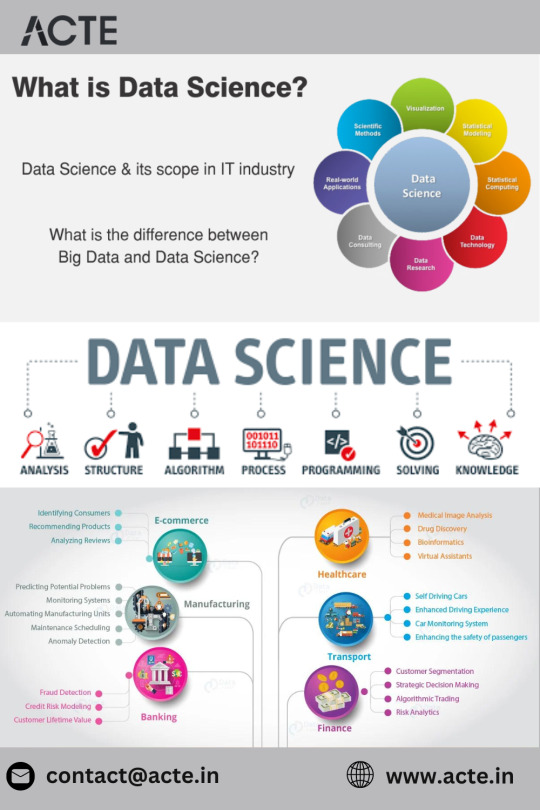

In the intricate tapestry of modern industries, data science stands as the master weaver, threading insights, predictions, and optimizations. From healthcare to finance, e-commerce to education, the applications of data science are as diverse as the sectors it transforms. Choosing the Top Data Science Institute can further accelerate your journey into this thriving industry. In this exploration, we'll embark on a journey to unravel the pervasive influence of data science across various domains, witnessing its transformative power and impact on decision-making in the digital age.

Healthcare: Pioneering Precision Medicine

In the healthcare sector, data science acts as a beacon of innovation. It plays a pivotal role in patient diagnosis, treatment optimization, and personalized medicine. By analyzing vast datasets, healthcare professionals can identify patterns, predict disease outcomes, and tailor treatments to individual patients. This not only enhances the efficiency of healthcare delivery but also contributes to groundbreaking advancements in medical research.

Finance: Navigating Risk and Detecting Fraud

The financial landscape is ripe for data science applications, particularly in risk management, fraud detection, and algorithmic trading. Data-driven models analyze market trends, assess risk exposure, and identify fraudulent activities in real-time. This not only safeguards financial institutions but also empowers them to make informed investment decisions, optimizing portfolios for better returns.

E-commerce: Crafting Personalized Experiences

In the bustling world of e-commerce, data science is the engine driving personalized experiences. Recommendation systems powered by data analysis understand user behavior, preferences, and purchase history. This results in tailored product suggestions, optimized pricing strategies, and a seamless shopping journey that boosts sales and enhances customer satisfaction.

Telecommunications: Enhancing Connectivity and Predicting Maintenance

Telecommunications companies leverage data science for network optimization, predictive maintenance, and customer churn analysis. By analyzing vast datasets, they can optimize network performance, predict potential issues, and proactively address concerns. This not only enhances the reliability of communication networks but also improves the overall customer experience.

Marketing: Precision in Targeting and Campaign Optimization

Marketers rely on data science for precision in targeting and campaign optimization. Customer segmentation, behavior analysis, and predictive modeling help marketers tailor their strategies for maximum impact. This ensures that marketing efforts are not only more effective but also cost-efficient, yielding higher returns on investment.

Education: Tailoring Learning Experiences

In the realm of education, data science is reshaping how students learn. Personalized learning experiences, performance analytics, and resource optimization are made possible through data analysis. By understanding student behavior and learning patterns, educators can tailor educational strategies to individual needs, fostering a more adaptive and effective learning environment.

Manufacturing: Predictive Maintenance and Quality Control

Manufacturing enterprises harness data science for predictive maintenance, quality control, and supply chain optimization. Analyzing data from sensors and production lines allows for predictive maintenance, minimizing downtime and reducing defects. This not only enhances operational efficiency but also contributes to cost savings. Choosing the best Data Science Courses in Chennai is a crucial step in acquiring the necessary expertise for a successful career in the evolving landscape of data science.

Energy: Sustainability and Operational Efficiency

Data science is a driving force in the energy sector, contributing to sustainability and operational efficiency. Predictive maintenance of equipment, analysis of energy consumption patterns, and optimization of energy production are facilitated through data-driven insights. This not only ensures reliable energy supply but also contributes to the global push for sustainable practices.

Transportation and Logistics: Optimizing Routes and Operations

In transportation and logistics, data science is instrumental in optimizing routes, predicting demand, and managing fleets efficiently. By analyzing data on traffic patterns, delivery times, and inventory levels, companies can optimize logistics operations, reduce costs, and improve overall service delivery.

Human Resources: Talent Acquisition and Workforce Planning

Human Resources (HR) departments utilize data science for talent acquisition, employee engagement analysis, and workforce planning. Analyzing data on employee performance, satisfaction, and recruitment processes enables HR professionals to make informed decisions, attract top talent, and optimize organizational performance.

Social Media: Enhancing User Engagement and Content Recommendation

Social media platforms leverage data science for enhancing user engagement and content recommendation. Algorithms analyze user interactions, preferences, and behaviors to recommend personalized content and improve overall user experience. This not only keeps users engaged but also enhances the platform's ability to deliver relevant content.

Government and Public Policy: Informed Decision-Making

In the realm of government and public policy, data science aids in informed decision-making. Analyzing data on various facets, including crime rates, resource allocation, and citizen services, enables governments to optimize policies for the welfare of the public. This data-driven approach enhances governance and contributes to more effective public services.

As we traverse the vast landscape of industries, it becomes evident that data science is not merely a tool but a transformative force that connects and elevates diverse sectors. Its ability to extract insights, predict outcomes, and optimize processes is reshaping the way businesses and institutions operate. In an era defined by data, data science stands as a thread weaving through the fabric of innovation, connecting industries and shaping the future of decision-making. As we continue to explore the frontiers of technology, the influence of data science is set to expand, leaving an indelible mark on the evolution of industries across the globe.

3 notes

·

View notes

Text

Transforming Digital Visions: A Leading Software Development Company at Your Service

In the fast-paced world of digital transformation, choosing the right software development company is crucial to staying ahead of the curve. Whether you're a startup looking to scale or an enterprise streamlining operations, tailored software solutions can significantly enhance your efficiency and user experience. This blog explores why Infograins stands out as a reliable technology partner and how our expertise adds value across industries.

Empowering Businesses Through Innovation

The future belongs to companies that innovate, adapt, and scale intelligently. At Infograins, we specialize in building powerful, scalable, and intelligent digital solutions. As a trusted custom software development company, we aim to bring your ideas to life through seamless technology integration. From ideation to deployment, our agile methodologies ensure that you always stay a step ahead of your competition.

Overview: Our Approach to Custom Software Development

We don’t believe in one-size-fits-all solutions. Instead, we focus on understanding your business goals, operational challenges, and end-user needs to craft tailored applications. Our core strength lies in delivering custom software development services that are scalable, secure, and aligned with your growth objectives. Be it enterprise software, SaaS products, or cloud-native applications—our team brings extensive domain expertise to deliver tangible business results.

Pros of Choosing Custom Software Development

Opting for custom-built software brings multiple benefits, including:

Scalability: Built to grow with your business.

Efficiency: Designed to automate and simplify operations.

Security: Advanced protocols tailored to your specific risk profile.

Integration: Seamlessly integrates with existing systems and third-party apps.

User-Centric: UI/UX designed with your target audience in mind.

With our custom software development services, you get full ownership, long-term cost savings, and strategic tech advantage.

Why Choose Infograins?

Infograins is more than just a service provider; we are a growth catalyst. Our team consists of seasoned developers, project managers, QA testers, and business analysts who ensure your project is delivered on time and within scope. We follow a consultative approach that emphasizes:

Thorough requirement analysis

Transparent communication

Agile development practices

Rigorous testing protocols

Post-launch support & optimization

Our consistent track record of successful implementations has made us a go-to custom software development company for clients across industries and geographies.

Infograins as Your Long-Term Tech Partner

Choosing the right development partner is not just about skills—it's about trust, accountability, and alignment. Infograins offers ongoing support, version upgrades, bug fixes, and performance tuning, ensuring your software continues to evolve. We believe in forming long-term partnerships by delivering measurable business value. From product roadmap planning to market launch, we walk with you every step of the way.

FAQs: Answers to Your Common Queries

1. What industries does Infograins serve with its custom software development? We cater to a diverse range of industries including healthcare, finance, eCommerce, logistics, education, real estate, and more.

2. How does Infograins ensure data security in software development? We follow industry best practices like encryption, secure APIs, role-based access control, and compliance with regulations such as GDPR and HIPAA.

3. What is the typical project delivery timeline? Timelines vary depending on complexity, but we follow agile sprints and provide clear milestone-based delivery schedules for transparency and predictability.

4. Can Infograins help modernize our existing legacy system? Yes, we specialize in legacy system modernization, helping businesses migrate to scalable and efficient digital infrastructures.

5. What makes Infograins different from other development companies? Our commitment to quality, transparent processes, long-term client relationships, and our proven expertise in custom software development services set us apart.

Conclusion

In an era where technology drives every business decision, choosing the right software development company can be the game-changer. Infograins is here to help you build robust, innovative, and scalable software solutions tailored to your unique needs. Let’s innovate together—your vision, our code.

0 notes

Text

Agri Nanotech Industry Forecast: US$ YY B by 2031

Market Size & Forecast

Introduction & Definition

Agricultural nanotechnology refers to the application of nanoscale technologies and materials in agriculture to enhance efficiency, sustainability, and yield. These include nano fertilizers, nano pesticides, nano-based seed treatments, biosensors for field diagnostics, and nano-enabled delivery systems for agrochemicals. These technologies reduce input waste, minimize environmental impact, and optimize resource use, making them key to modern precision farming.

Market Drivers & Restraints

Drivers:

Rising demand for precision agriculture solutions that increase productivity with minimal input

Adoption of nano-based fertilizers and pesticides for targeted delivery and reduced environmental impact

Growing investment in smart farming and agricultural R&D

Favorable government policies promoting sustainable agricultural innovations

Restraints:

High initial cost of nanotech-enabled inputs

Regulatory uncertainty concerning the long-term ecological effects of nanomaterials

Limited awareness and accessibility among smallholder farmers in emerging economies To get a free sample report, click on https://www.datamintelligence.com/download-sample/agricultural-nanotechnology-market.

Segmentation Analysis

Nano Fertilizers: Among the fastest-growing segments due to their ability to deliver nutrients directly to plant roots in a controlled-release manner.

Nano Pesticides and Herbicides: Enable targeted pest control, reducing chemical runoff and ecological disruption.

Nano Biosensors: Play a critical role in real-time monitoring of soil nutrients, pathogens, and environmental stress.

Other Applications: Include nano-enabled packaging, plant breeding enhancements, and nanomaterials for soil restoration. To get the unlimited market intelligence, subscribe to https://www.datamintelligence.com/reports-subscription

Geographical Insights

North America: Leads global adoption due to advanced agricultural infrastructure and strong R&D presence.

Europe: A rapidly growing market driven by sustainability goals and innovation in precision farming.

Asia-Pacific: Shows significant potential, especially in countries like India, China, and Japan, where agricultural transformation is underway.

Latin America & Middle East: Emerging opportunities driven by growing food demand and investments in modern farming technologies.

Recent Trends & Industry Highlights

Smart nano-fertilizers: Featuring micronutrient encapsulation for improved crop uptake.

Nano-encapsulation technology: Extending the shelf life and improving the efficiency of agrochemicals.

Integration with AI and IoT: For smart sensing and decision-making in crop management.

Nanobubble irrigation: Enhancing water use efficiency and soil oxygenation.

Biodegradable nanomaterials: Offering safer environmental profiles and eco-friendly alternatives to conventional inputs.

Competitive Landscape

Prominent companies in the Agricultural Nanotechnology space include:

Aqua-Yield

Coromandel International

NanoSpy

NanoScale Corp

Indogulf BioAg

Nanoco Group

Nanoshell These companies are involved in manufacturing nano fertilizers, nano pesticides, diagnostic biosensors, and nano-formulated crop care products, all focused on improving agricultural productivity and sustainability.

Key Developments

New product launches of nano zinc and nano copper fertilizers for correcting micronutrient deficiencies

Expanded R&D into nanopriming and seed coating technologies for climate-resilient farming

Increasing collaborations between universities and agri-tech firms to develop biodegradable and eco-safe nanoparticles

Policy discussions around safe deployment and labeling of nanomaterials in agriculture in both developed and developing markets

Report Features & Coverage

This comprehensive report includes:

Historical and forecasted market sizing and growth trends

Detailed segmentation analysis by product, application, and region

Competitive benchmarking and company profiling

Technology landscape and innovation mapping

Regional and policy outlook with investment opportunities

Challenges, risks, and future trends in nanotechnology for agriculture

About Us

DataM Intelligence is a global research and consulting firm specializing in emerging technologies, including nanotechnology and smart agriculture. Our data-driven insights support business leaders, innovators, and policymakers in making informed decisions across the global agricultural value chain.

Contact Us

To access the full Agricultural Nanotechnology Market report or to speak with an analyst: Email: [email protected] Phone: +1‑877‑441‑4866

0 notes

Text

US and Japan Biotech Investment Propels Electroporation Demand

The Electroporation Instruments and Consumables Market is witnessing robust growth, driven by increasing applications in gene therapy, DNA and mRNA vaccine delivery, and precision biotechnology research. Electroporation technology enables controlled delivery of nucleic acids, drugs, and proteins into cells, making it an essential tool in both academic and clinical settings.

To Get Free Sample Report: https://www.datamintelligence.com/download-sample/electroporation-instruments-and-consumables-market

Market Size & Future Outlook

Valued at approximately USD 212.5 million in 2020, the electroporation instruments and consumables market is projected to reach around USD 350.8 million by 2028, growing at a compound annual growth rate (CAGR) of 6.8%. North America currently dominates the market with an estimated 38–40% global share, thanks to its mature biotechnology sector, strong clinical pipeline, and supportive research funding. Meanwhile, Asia-Pacific is forecasted to be the fastest-growing region, with rising investments in biotechnology and growing demand for genetic engineering solutions.

Key Market Drivers

1. Expansion in Gene Therapy and Vaccine Research Electroporation has become an indispensable method for DNA and RNA vaccine delivery. Its use enhances transfection efficiency and enables more consistent immune responses. The COVID-19 pandemic significantly accelerated its adoption in vaccine research and delivery technologies.

2. Adoption in Monoclonal Antibody Production The growing burden of autoimmune diseases, cancer, and viral infections has driven demand for monoclonal antibodies. Electroporation plays a critical role in antibody development and high-throughput screening.

3. Integration with CRISPR and Gene Editing Tools CRISPR-Cas9 and other gene-editing technologies rely on precise cellular delivery systems. Electroporation instruments provide the control needed to introduce gene editors into both somatic and stem cells.

4. Growth in Biotech Research Funding Increased government and private funding in genomic research, cell therapy, and bioengineering is bolstering demand for both instruments and consumables used in electroporation workflows.

5. Automation and Scalability Integration with automated platforms and high-throughput systems has made electroporation scalable and reproducible. Innovations in electroporator designs are expanding their usability in both small labs and large biopharma companies.

Segment Insights

Instruments Electroporation instruments, including systems designed for microbial, plant, and mammalian cells, are the backbone of the market. These devices enable precise pulse control, ensuring high efficiency and cell viability.

Consumables Consumables like cuvettes, electrodes, buffers, and electroporation plates represent over 55% of the market share. Their recurring nature makes them vital for daily lab operations. As labs scale experiments or move to GMP-compliant environments, the demand for high-quality consumables increases.

Regional Analysis

United States The US continues to dominate the market, driven by clinical trials, therapeutic development, and robust R&D activities. Companies such as Thermo Fisher Scientific, MaxCyte, and Bio-Rad Laboratories are leading product innovation. The US biotech ecosystem encourages the use of advanced electroporation systems, especially in cancer research, CAR-T cell therapy, and next-gen vaccine platforms.

Japan Japan’s market is growing steadily, supported by national strategies focused on regenerative medicine and aging-related therapies. The country's focus on precision medicine and investments in gene-editing technologies position it as a strong contributor in the Asia-Pacific electroporation segment. Japanese manufacturers are also developing compact, high-efficiency systems suited to domestic and regional research institutions.

Emerging Trends and Innovation

Pulsed-Field Electroporation Systems These systems offer controlled energy delivery and are especially useful for transfecting hard-to-reach cell types, such as neurons and stem cells.

Microprocessor-Controlled Devices Offering programmable settings, these devices deliver precision for different cell types and experiment protocols, gaining wide usage in laboratories globally.

Nanotechnology in Electroporation Integration of nanocarriers with electroporation enhances delivery specificity and reduces off-target effects.

Reagent and Buffer Advancements Next-gen electroporation buffers now increase transfection efficiency and reduce cytotoxicity, expanding the technology’s viability in sensitive applications.

Challenges & Constraints

High Cost of Equipment Electroporation devices and their consumables can be cost-prohibitive for small labs, especially in emerging economies.

Technical Expertise Requirement Proper setup and calibration are critical for successful use, necessitating skilled operators and standardized training.

Competing Technologies Other transfection techniques, including viral vectors, lipofection, and microinjection, remain strong competitors in gene and protein delivery.

Regulatory Hurdles Medical applications require strict regulatory compliance, especially in clinical-grade gene therapies, which can delay product approvals.

Competitive Landscape

The competitive space is shaped by both global leaders and emerging players. Companies such as Thermo Fisher Scientific, MaxCyte, Bio-Rad Laboratories, Eppendorf, Lonza, Mirus Bio, Harvard Bioscience, Celetrix LLC, and BEX Co. Ltd are among the key innovators.

Recent product developments include:

Thermo Fisher's Xenon electroporation platform for large-volume cell therapy applications

MaxCyte’s Flow Electroporation technology for non-viral, scalable delivery in clinical pipelines

Mirus Bio’s Ingenio System, widely used for high-efficiency research-grade applications

These firms are expanding into personalized medicine, synthetic biology, and high-efficiency immunotherapy.

Subscribe for Insights: https://www.datamintelligence.com/reports-subscription

Market Outlook

As gene therapies, cell-based treatments, and vaccine innovations evolve, the electroporation instruments and consumables market will remain a key enabler of precision medicine. Analysts expect the market to cross USD 400 million within the next decade, driven by rising clinical applications and the need for scalable, safe transfection methods.

Asia-Pacific, led by Japan, China, and South Korea, is expected to post the highest growth, while North America will retain its market leadership through continuous innovation.

Final Thought

The electroporation instruments and consumables market is transitioning from a research-only tool to a clinical-scale, therapy-enabling platform. With increasing investments in biotech, breakthroughs in gene delivery, and expanding global access, the market is poised for a transformative decade.

Firms that invest in automation, consumables innovation, and user-friendly system designs will lead the next phase of growth in this high-impact domain.

0 notes

Text

Pilot Air Control Valves Market: Cost-Benefit Analysis for Infrastructure Projects

MARKET INSIGHTS

The global Pilot Air Control Valves Market size was valued at US$ 2,340 million in 2024 and is projected to reach US$ 3,870 million by 2032, at a CAGR of 7.51% during the forecast period 2025-2032. The U.S. market accounted for 28% of global revenue in 2024, while China is expected to grow at a faster CAGR of 6.7% through 2032 due to increasing industrial automation.

Pilot Air Control Valves are precision pneumatic components that regulate compressed air flow in industrial systems through pilot-operated mechanisms. These valves are categorized into 2-way, 3-way, and 4-way configurations, each designed for specific directional control applications in pneumatic circuits. The 2-way segment currently dominates with over 42% market share, driven by widespread use in basic on/off applications across manufacturing facilities.

The market growth is primarily fueled by accelerating industrial automation across sectors, particularly in automotive and electronics manufacturing. However, supply chain disruptions for raw materials like aluminum and brass have created pricing pressures. Key players including Parker Hannifin and SMC Corporation are addressing these challenges through strategic acquisitions – Parker’s 2023 purchase of Clippard strengthened its position in miniature valve solutions, while SMC expanded its Asian production capacity by 15% in early 2024 to meet growing regional demand.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Industrial Automation to Accelerate Pilot Air Control Valve Adoption

The global industrial automation sector is experiencing unprecedented growth, with investments projected to exceed $400 billion annually by 2030. Pilot air control valves serve as critical components in automated pneumatic systems, enabling precise regulation of air pressure and flow in manufacturing processes. This surge in automation adoption across industries ranging from automotive to food processing is directly translating to increased demand for high-performance control valves. The valves’ ability to ensure operational efficiency while minimizing energy consumption makes them indispensable in modern automated facilities. Furthermore, stringent quality standards in industries such as pharmaceuticals and electronics manufacturing are compelling organizations to upgrade their pneumatic systems with advanced control valve solutions.

Aerospace Sector Modernization to Fuel Valve Demand

The aerospace industry is undergoing significant fleet modernization efforts, with aircraft manufacturers increasing production rates to meet rebounding post-pandemic travel demand. Pilot air control valves play crucial roles in aircraft systems including cabin pressure regulation, landing gear operation, and auxiliary power units. With commercial aircraft deliveries expected to grow at 7% CAGR through 2030, component suppliers are facing tremendous pressure to scale production. The valves’ lightweight construction and reliability under extreme conditions make them particularly valuable in aerospace applications. Additionally, the expansion of space exploration programs worldwide is creating new opportunities for specialized valve solutions capable of performing in zero-gravity environments.

➤ For instance, recent advancements in additive manufacturing have enabled production of control valves with 40% weight reduction while maintaining structural integrity for aerospace applications.

MARKET RESTRAINTS

Supply Chain Disruptions to Impact Market Growth

While demand continues to accelerate, the pilot air control valve market faces significant supply-side challenges. The industry remains vulnerable to global supply chain disruptions affecting raw material availability, particularly for specialized alloys and precision components. Recent geopolitical tensions have exacerbated lead times for critical materials, with some manufacturers reporting 60-90 day delays in component deliveries. These disruptions are forcing companies to either carry higher inventory levels or redesign products to accommodate available materials – both approaches increasing production costs. Smaller manufacturers without diversified supplier networks are especially vulnerable to these market pressures.

Other Restraints

Price Sensitivity in Emerging Markets

Cost competitiveness remains a significant barrier in price-sensitive regions where end-users often prioritize initial purchase price over total cost of ownership. This creates challenges for manufacturers attempting to introduce advanced valve solutions with superior longevity and efficiency characteristics.

Regulatory Compliance Burdens

Increasing environmental and safety regulations across multiple jurisdictions require continuous product recertification, adding to development timelines and compliance costs for manufacturers operating in global markets.

MARKET CHALLENGES

Technological Specialization Straining Workforce Development

The industry faces a critical shortage of skilled technicians capable of designing, manufacturing, and maintaining increasingly sophisticated pilot air control valve systems. As valve technology incorporates more electronic components and smart capabilities, the required skill sets have expanded beyond traditional mechanical engineering. Training programs have struggled to keep pace with these evolving requirements, resulting in talent gaps particularly in specialized areas like materials science and fluid dynamics simulation. The challenge is compounded by an aging workforce, with many experienced valve engineers approaching retirement without adequate successors in place.

Other Challenges

Integration With IIoT Systems The rapid adoption of Industrial Internet of Things (IIoT) technologies presents both opportunities and challenges. While smart valve solutions promise enhanced monitoring and predictive maintenance capabilities, many legacy industrial facilities lack the infrastructure to support these advanced systems.

Precision Engineering Requirements Modern applications demand valves with micron-level precision and extremely tight tolerances, pushing manufacturing capabilities to their limits and requiring substantial investments in production equipment upgrades.

MARKET OPPORTUNITIES

Emergence of Smart Factory Concepts to Drive Next-Generation Valve Development

The transition toward Industry 4.0 is creating significant opportunities for innovation in pilot air control valve technology. Smart valves equipped with sensors, wireless connectivity, and embedded diagnostics are increasingly becoming integral components of connected manufacturing environments. These intelligent systems enable real-time performance monitoring, predictive maintenance, and automatic adjustments to optimize energy efficiency. Market leaders are investing heavily in R&D to develop valves that can seamlessly integrate with digital twin simulations and autonomous control systems. The predictive maintenance segment alone for industrial valves is projected to grow at nearly 20% CAGR through the decade, representing a major growth avenue for forward-thinking manufacturers.

Expansion in Emerging Economies Opens New Growth Frontiers

Rapid industrialization across developing markets presents substantial expansion opportunities. Countries in Southeast Asia and Africa are investing heavily in manufacturing infrastructure, with Indonesia, Vietnam, and Nigeria emerging as particularly promising markets. These regions offer attractive growth potential due to lower market saturation and increasing domestic capability to support industrial operations. Local production initiatives in these markets also create opportunities for technology transfer and joint venture partnerships. Strategic geographic expansion combined with product adaptations to meet regional requirements could yield significant returns for valve manufacturers.

PILOT AIR CONTROL VALVES MARKET TRENDS

Industry 4.0 Integration Revolutionizing Pilot Air Control Valve Market

The adoption of Industry 4.0 technologies is transforming the pilot air control valves market, particularly in industrial automation applications. Smart valves with integrated IoT sensors now account for over 30% of new installations in developed markets, enabling real-time pressure monitoring and predictive maintenance. These advanced valves reduce downtime by up to 40% while improving energy efficiency in pneumatic systems. Manufacturers are increasingly incorporating wireless connectivity features, with the industrial sector showing 25% year-over-year growth in demand for networked valve solutions. The transition towards digital factories has created substantial opportunities for intelligent valve systems that can integrate with broader automation architectures.

Other Trends

Energy Efficiency Standards Driving Product Innovation

Stricter global energy regulations are compelling manufacturers to develop more efficient pilot air control valve designs. New ceramic-sealed valves have demonstrated 15-20% better energy retention compared to traditional metal-seated models, particularly in high-cycle applications. The European Union’s Ecodesign Directive has accelerated development of low-leakage valves, with the commercial building sector showing particular interest in these solutions. Furthermore, compact valve designs with reduced internal volume now account for nearly 45% of the aerospace market segment, where weight and energy savings are critical performance factors.

Material Science Advancements Enhancing Valve Performance

Recent breakthroughs in materials engineering are significantly improving the durability and functionality of pilot air control valves. The commercial introduction of graphene-enhanced polymer composites has extended valve lifespans by 3-5 times in high-wear applications. Meanwhile, high-performance alloys resistant to corrosion now enable reliable valve operation in harsh environments, driving adoption in oil and gas applications. The market has seen particular growth in ultra-clean valves for semiconductor manufacturing, where particle generation must be minimized. These material innovations are particularly impactful in the 3-way valve segment, which represents about 32% of total market value.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Focus on Innovation & Regional Expansion to Capture Market Share

The global Pilot Air Control Valves market exhibits a moderately fragmented competitive landscape, with established industrial automation giants competing alongside specialized pneumatic component manufacturers. Parker Hannifin Corporation maintains a dominant position, commanding approximately 18% of the 2024 market revenue share due to its comprehensive product range spanning 2-way, 3-way, and 4-way valve configurations.

Emerson Electric Co. and SMC Corporation collectively held nearly 27% of the global market last year. Their strong performance stems from vertical integration capabilities and extensive distribution networks across industrial and aerospace sectors. Emerson’s recent acquisition of pneumatic component startups has particularly strengthened its IoT-enabled valve offerings.

While these industry leaders continue to dominate, mid-sized players like Festo and NUMATICS are gaining traction through niche specialization. Festo’s energy-efficient valve designs have captured 9% of the European market, whereas NUMATICS saw 12% year-over-year growth in North America through customized industrial solutions.

Meanwhile, Asian manufacturers such as AirTAC and KOGANEI Corporation are disrupting pricing structures. AirTAC’s 2023 financial reports indicate a 23% production cost advantage over Western counterparts, enabling aggressive expansion in emerging markets. However, trade barriers and quality perception challenges continue to limit their premium segment penetration.

List of Key Pilot Air Control Valve Manufacturers

Parker Hannifin Corporation (U.S.)

Emerson Electric Co. (U.S.)

SMC Corporation (Japan)

NITRA Pneumatics (Slovakia)

Pneumadyne, Inc. (U.S.)

NUMATICS (U.S.)

Clippard Instrument Laboratory, Inc. (U.S.)

ARO (Ingersoll Rand) (U.S.)

Humphrey Products (U.S.)

Festo (Germany)

KOGANEI Corporation (Japan)

AirTAC (Taiwan)

The competitive intensity continues to rise as manufacturers balance performance enhancements with cost reduction pressures. While industrial applications drive volume sales, aerospace-grade valves generate higher margins, prompting firms to develop dual-certification products. Recent developments show established players forming technology partnerships with automation software providers to deliver smart valve solutions, whereas regional specialists focus on distribution network expansions.

Segment Analysis:

By Type

2-Way Segment Leads Due to Wide Adoption in Industrial Automation

The market is segmented based on type into:

2-Way

Subtypes: Normally Open, Normally Closed

3-Way

4-Way

By Application

Industrial Applications Dominate Market Share Owing to High Demand in Manufacturing Processes

The market is segmented based on application into:

Industrial

Subtypes: Pneumatic Systems, Process Control

Aerospace

Others

By Material

Brass Segment Holds Largest Market Share Due to Corrosion Resistance Properties

The market is segmented based on material into:

Brass

Stainless Steel

Aluminum

Plastic

By End-Use Industry

Manufacturing Sector Accounts for Significant Market Share

The market is segmented based on end-use industry into:

Oil & Gas

Chemical Processing

Food & Beverage

Pharmaceutical

Others

Regional Analysis: Pilot Air Control Valves Market

North America The North American market for pilot air control valves is driven by advanced manufacturing practices and strict industrial automation standards. The U.S. accounts for the largest share within the region, supported by strong demand from the aerospace and industrial sectors—key end-users of precision pneumatic components. Regulatory standards, such as ASME B16.34, ensure product reliability, which further boosts adoption. Critical infrastructure projects, including energy and automation, propel demand. However, pricing pressures due to competition from Asian manufacturers pose challenges. Major players like Parker and Emerson dominate through continuous innovation in valve efficiency and smart control integration.

Europe Europe emphasizes energy-efficient pneumatic solutions, aligning with EU Green Deal initiatives targeting carbon-neutral industries. Germany and France lead the regional market due to their robust manufacturing bases, particularly in automotive and industrial automation. Stringent environmental norms accelerate the shift toward low-emission pneumatic valves, with companies like Festo and SMC Corporation investing in sustainable designs. The growing adoption of Industry 4.0 practices supports smart valve integration. However, high production costs and economic uncertainties in Eastern Europe moderate growth. Collaborative R&D efforts between universities and manufacturers drive technological advancements.

Asia-Pacific Asia-Pacific represents the fastest-growing market, led by China’s massive industrial expansion and Japan’s dominance in high-precision valve manufacturing. The region benefits from cost-competitive production and rising automation across industries like electronics and automotive. SMC Corporation and AirTAC hold significant market shares due to localized production advantages. While 3-way and 4-way valves dominate industrial applications, infrastructure investments in Southeast Asia open new opportunities. Challenges include inconsistent quality standards and intellectual property concerns. Government initiatives to enhance manufacturing capabilities, such as India’s “Make in India”, further fuel regional demand.

South America South America experiences steady growth, supported by Brazil’s industrial sector and mining applications. The adoption of modular pneumatic systems in food processing and agriculture drives demand. However, economic instability and currency fluctuations limit large-scale investments, leading to reliance on imports. Local manufacturers focus on cost-effective solutions, but technological gaps persist. Infrastructure projects in Argentina and Colombia may create opportunities, though political uncertainties slow market expansion. Partnerships with global players aim to improve technical capabilities in valve automation.

Middle East & Africa The MEA market remains nascent but promising, driven by oil & gas and water management applications. The UAE and Saudi Arabia lead with smart city projects requiring advanced pneumatic controls. High dependency on imports and limited local expertise hinder rapid adoption, though governments are incentivizing industrial diversification. Demand for durable valves in harsh environments presents growth potential. Regional players face challenges in competing with global suppliers due to budget constraints. Long-term infrastructure plans, like Saudi Arabia’s Vision 2030, are expected to gradually boost the market.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Pilot Air Control Valves markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 287.5 million in 2024 and is projected to reach USD 398.2 million by 2032 at a CAGR of 4.8%.

Segmentation Analysis: Detailed breakdown by product type (2-Way, 3-Way, 4-Way), application (Industrial, Aerospace, Others), and end-user industry to identify high-growth segments and investment opportunities. The 2-Way segment is expected to dominate with over 42% market share by 2032.

Regional Outlook: Insights into market performance across North America (U.S. market size estimated at USD 78.4 million in 2024), Europe, Asia-Pacific (China projected to reach USD 112.6 million by 2032), Latin America, and the Middle East & Africa, including country-level analysis where relevant.

Competitive Landscape: Profiles of leading market participants including Parker, Emerson, SMC Corporation, NITRA, and Pneumadyne, Inc., covering their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships. The top five players held approximately 58% market share in 2024.

Technology Trends & Innovation: Assessment of emerging technologies in valve automation, smart control systems, IoT integration, and evolving industry standards for pneumatic systems.

Market Drivers & Restraints: Evaluation of factors driving market growth (industrial automation, aerospace sector expansion) along with challenges (supply chain constraints, raw material price volatility).

Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in the pneumatic control systems market.

Related Reports:https://semiconductorblogs21.blogspot.com/2025/06/laser-diode-cover-glass-market-valued.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/q-switches-for-industrial-market-key.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/ntc-smd-thermistor-market-emerging_19.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/lightning-rod-for-building-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/cpe-chip-market-analysis-cagr-of-121.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/line-array-detector-market-key-players.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/tape-heaters-market-industry-size-share.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/wavelength-division-multiplexing-module.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/electronic-spacer-market-report.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/5g-iot-chip-market-technology-trends.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/polarization-beam-combiner-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/amorphous-selenium-detector-market-key.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/output-mode-cleaners-market-industry.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/digitally-controlled-attenuators-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/thin-double-sided-fpc-market-key.html

0 notes

Text

High-Quality Benzylhydrazine Dihydrochloride by Jay Finechem

Benzylhydrazine dihydrochloride (CAS No. 20570-96-1) is a key intermediate in pharmaceutical and organic chemical synthesis. Known for its reactivity and role in preparing active pharmaceutical ingredients, it demands high standards of purity and consistency. Jay Finechem, a reputed Indian chemical company, is a trusted Benzylhydrazine dihydrochloride manufacturer, offering premium-grade material tailored to industrial needs.

Jay Finechem’s expertise in producing niche fine chemicals ensures reliable quality, technical accuracy, and compliance with global regulatory expectations. This makes them one of the most preferred Benzylhydrazine dihydrochloride suppliers for pharmaceutical companies and research institutions worldwide.

CAS No. 20570-96-1 Manufacturer with Global Standards

As a recognized CAS No. 20570-96-1 manufacturer, Jay Finechem delivers Benzylhydrazine dihydrochloride with consistent specifications and complete documentation, including a Certificate of Analysis (COA) and MSDS. The company’s processes are governed by GMP-compliant practices, allowing customers to trust the quality at every stage of procurement and application.

Their R&D-backed approach and stringent quality checks ensure that the chemical meets the exact parameters required for laboratory research and API development. This commitment to excellence positions them among the leading CAS No. 20570-96-1 suppliers in the global fine chemical market.

Leading Indian Supplier of Benzylhydrazine Dihydrochloride

Operating from Vapi, Gujarat, a prominent industrial zone, Jay Finechem stands out as a top CAS No. 20570-96-1 Indian manufacturer. Their location gives them a strategic advantage in terms of raw material sourcing, compliance infrastructure, and timely logistics.

As a Benzylhydrazine dihydrochloride manufacturer in India, Jay Finechem combines modern production capabilities with a strong emphasis on safety, environmental compliance, and scalability. Whether you are looking for lab-scale quantities or bulk production, the company provides reliable solutions tailored to customer requirements.

Trusted Benzylhydrazine Dihydrochloride Supplier in Vapi and Across India

Jay Finechem is not only a major Benzylhydrazine dihydrochloride Vapi-based supplier but also serves clients across the country and abroad. Their dedicated technical team offers full customer support from inquiry to delivery. Clients appreciate their transparent dealings, stable pricing, and consistent product availability.

For industries looking to buy Benzylhydrazine dihydrochloride in India, Jay Finechem is a dependable source for purity, compliance, and timely delivery. As an established Benzylhydrazine dihydrochloride supplier in India, the company supports both domestic industries and global exporters with competitive pricing and top-tier customer service.

Why Choose Jay Finechem?

CAS No. 20570-96-1 supplier with stringent quality control

In-house testing labs and documentation for every batch

Efficient logistics from Vapi, a chemical manufacturing hub

Reliable bulk and custom packaging options

Whether you're a pharma company, research lab, or international distributor, Jay Finechem is your trusted Benzylhydrazine dihydrochloride manufacturer in India, delivering uncompromised quality and professional service.

0 notes

Text

Growth of Application Delivery Controller Market: Key Drivers and Challenges

The global Application Delivery Controller (ADC) market was valued at USD 4.35 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 12.9% from 2025 to 2030. Application Delivery Controllers (ADCs) play a crucial role in managing and optimizing the delivery of applications across complex IT environments. These solutions ensure that applications are available, secure, and perform well under varying conditions. Initially, ADCs were primarily used for traffic balancing between servers to improve the distribution of requests. However, modern ADC solutions have evolved to incorporate a broader range of functionalities. These include application acceleration, SSL offloading, Web Application Firewalls (WAFs), and advanced protection against Distributed Denial of Service (DDoS) attacks, all of which are crucial in safeguarding applications and ensuring a smooth user experience.

The rise in cyber threats globally has made application security a top priority for organizations across various industries. With more organizations embarking on digital transformation initiatives, the need for secure, high-performance application delivery is intensifying. As businesses continue to adopt more cloud-based architectures and seek greater scalability and flexibility, the demand for cloud-native ADCs has also risen. These solutions are specifically designed to cater to dynamic workloads, and multi-cloud environments, enabling organizations to scale rapidly while maintaining application performance and security. Furthermore, businesses are becoming increasingly focused on enhancing application performance and improving user experience. To address these demands, advanced ADCs are incorporating cutting-edge technologies such as Artificial Intelligence (AI) and Machine Learning (ML). These technologies enable ADCs to conduct predictive analytics and automate traffic management, allowing the systems to adapt to changing traffic patterns and optimize resource allocation in real-time. This helps organizations ensure that applications remain responsive, secure, and reliable under varying network conditions.

Gather more insights about the market drivers, restrains and growth of the Application Delivery Controller Market

Enterprise Size Insights

In 2024, large enterprises accounted for the largest share of the ADC market. Large enterprises typically manage complex IT environments that combine a mix of on-premises, cloud, and hybrid architectures. This level of complexity presents significant challenges for managing application delivery, traffic distribution, and security. As a result, large organizations require sophisticated solutions that can handle a wide variety of infrastructures and workloads. ADCs are specifically designed to address these challenges by providing centralized control over application traffic, enabling seamless integration across different platforms, and ensuring that applications remain highly available and secure across all environments. Additionally, ADCs improve operational efficiency by simplifying the management of diverse applications. They allow organizations to monitor and optimize performance from a single point of control, making it easier to manage the flow of traffic and ensure that each application receives the resources it needs to function optimally.

For large enterprises, ADCs are indispensable tools in navigating complex IT landscapes. Their ability to balance traffic, ensure high availability, and implement security measures across multiple environments is critical in maintaining smooth, uninterrupted application delivery. As organizations face growing complexities in their IT infrastructures, the demand for ADC solutions is expected to continue rising. These advanced tools are becoming essential for large enterprises striving to maintain high performance, scalability, and security across their increasingly intricate digital ecosystems.

Small and Medium Enterprise (SME) Insights

The SME segment is anticipated to experience steady growth over the forecast period. As small and medium enterprises (SMEs) continue to embrace digital transformation, the demand for application delivery solutions is increasing. Many SMEs are adopting cloud services to improve their operational efficiency and enhance customer engagement. With cloud adoption, SMEs are now able to access resources more flexibly and cost-effectively, which has created a growing need for reliable, high-performance application delivery solutions.

ADCs play a vital role in this digital transition by ensuring reliable and efficient access to applications across various platforms. They help optimize performance, minimize latency, and reduce downtime, all of which significantly enhance the user experience for both employees and customers. As SMEs increasingly recognize the importance of digital strategies to stay competitive in the market, ADCs have become a crucial part of their digital infrastructure.

These solutions not only provide seamless application delivery but also support scalability and adaptability, enabling SMEs to rapidly scale their operations in response to changing market demands. In today’s fast-paced business environment, where market dynamics are constantly shifting, the ability to quickly adapt and meet customer needs is essential. As SMEs embark on their digital transformation journeys, the demand for ADCs is expected to grow, allowing them to streamline their operations, improve performance, and better compete in an increasingly digital world.

Order a free sample PDF of the Application Delivery Controller Market Intelligence Study, published by Grand View Research.

#Application Delivery Controller Market#Application Delivery Controller Market Analysis#Application Delivery Controller Market Report#Application Delivery Controller Industry

0 notes

Text

Material Handling Equipment Market Outlook Global Trends, Statistics, Size, Share, Regional Analysis by Key Players (2021-2031)

The Material handling equipment market size is expected to reach US$ 92.63 billion by 2031 from US$ 60.05 billion in 2024. The market is estimated to record a CAGR of 6.51% from 2025 to 2031.

Executive Summary and Global Market Analysis

The global material handling equipment market is experiencing strong growth. This is largely due to rapid industrialization, increased warehouse automation, and the expanding e-commerce sector. The market includes a wide array of equipment used for transporting, storing, controlling, and protecting materials throughout various processes, including manufacturing, distribution, and disposal.

The industry's expansion is primarily driven by a growing need for operational efficiency, the increasing adoption of automation technologies, and a demand for better supply chain transparency. In response, manufacturers are developing innovative solutions that integrate advanced technologies like artificial intelligence (AI), the Internet of Things (IoT), and robotics to optimize warehouse operations and logistics infrastructure. Geographically, the Asia-Pacific region leads the market, thanks to significant infrastructure investments and rapid urbanization in countries like China and India.

Download our Sample PDF Report

@ https://www.businessmarketinsights.com/sample/BMIPUB00031690

Material Handling Equipment Market Segmentation Analysis

The material handling equipment market analysis is derived from key segments: technology, material, application, and end user.

By Equipment Type, the market is segmented into:

Cranes and Lifting Equipment

Industrial Trucks

Automated Storage and Retrieval Systems (AS/RS)

Conveying Systems

Racking and Storage Equipment

Automated Guided Vehicles (AGVs)

Bulk Material Handling Equipment

Others

By End-Use Industry, the market is segmented into:

Logistics

Automotive

Construction

Food & Beverages

Pharmaceuticals/Healthcare

Semiconductor & Electronics

By Application Type, the market is segmented into:

Assembly

Transportation

Distribution

Others

Material Handling Equipment Market Drivers and Opportunities

The rapid expansion of e-commerce is a significant driver for the material handling equipment market. As online retail grows, companies like Amazon and Alibaba are investing in automated warehouses to manage high order volumes. This, in turn, increases the demand for equipment such as forklifts, conveyors, and Automated Guided Vehicles (AGVs).

Urbanization and rising consumer expectations for quick deliveries further boost the need for efficient logistics systems. The growth of warehousing in regions like Asia-Pacific and North America directly fuels equipment sales. As e-commerce continues its upward trend, the demand for advanced material handling solutions to streamline operations and reduce delivery times will significantly propel market expansion.

Material Handling Equipment Market Size and Share Analysis

By Equipment Type: Cranes and Lifting Equipment, along with Industrial Trucks, Automated Storage and Retrieval Systems (AS/RS), Conveying Systems, Racking andStorage Equipment, Automated Guided Vehicles (AGVs), and Bulk Material Handling Equipment, are crucial. Cranes and lifting equipment are vital across construction, manufacturing, heavy engineering, automotive, and logistics for efficiently moving heavy materials and payloads. The construction industry, in particular, drives substantial demand due to ongoing urbanization, infrastructure development, and large-scale industrial projects.

By End-User Industry: The global growth of automobile production necessitates efficient material handling systems to manage the flow of materials and finished vehicles within factories and distribution centers. Automotive manufacturing plants are increasingly adopting modernized material handling infrastructure to improve assembly processes, reduce turnaround times, and support lean manufacturing principles, all of which require advanced handling equipment. The automotive industry's adoption of automation, robotics, and IoT-enabled material handling solutions enhances operational efficiency and safety, further boosting the demand for sophisticated equipment.

About Us: